Affiliate Disclosure: Automoblog and its partners may earn a commission if you purchase a plan from the car insurance providers outlined here. These commissions come to us at no additional cost to you. Our research team has carefully vetted dozens of car insurance providers. See our Privacy Policy to learn more.

Crash Course:

- Learn the best way to shop for car insurance.

- Discover how and where to find the best auto insurance rates.

- Learn what to look for in a provider and see two of the ones we recommend.

Unless you live in New Hampshire or Virginia where auto coverage isn’t required, you’ll have to shop for car insurance at some point. Why not do it the right way? To help you find the right provider that offers you the coverage you want at the best price, we’ve put together this guide.

Inside, you’ll find some key information to help you understand what to look for in a policy and a provider. We’ve also included some tips on insurance shopping strategies so you can more easily find the best rates available. You’ll also find a few recommendations for a couple of the best car insurance companies from our most recent industry-wide auto insurance study.

How To Shop For Car Insurance: 5 Easy Steps

The best way to shop for auto coverage is to be organized, have a clear plan, and carefully evaluate your options before choosing a provider and plan. By following just a few simple steps, you’ll have the best chance of finding the coverage you want from a quality provider at the lowest rates.

1. Gather Your Information

Before you start shopping around for an auto policy, it helps to get organized. Getting everything you need together first helps to ensure an efficient process and that you’ll get accurate quotes.

What Information Do You Need to Shop For Car Insurance?

Insurance companies use a few pieces of information about you and your vehicle to determine your rates. Before you shop for car insurance, it’s a good idea to get all this information in one place for easy access.

Here’s what to prepare:

- Information about your vehicle: You’ll need to know your car’s make, model, year, and mileage. It’s also helpful to have your vehicle identification number (VIN) handy. This number is located in several places on your vehicle, typically including inside the driver’s side door jamb, on the engine block, and on where your dashboard meets your windshield behind your steering wheel.

- Personal information: Insurance companies may ask you to provide your full name, date of birth, address, and driver’s license number. If you’re a student or you’ve served in the military, this could get you a discount, so be prepared to mention this as well

- Driving record: Your driving history is an important factor in your rates. You’ll want to be as accurate as possible when requesting quotes since your insurer will have access to your official record. Consider whether you have had any accidents or traffic violations in the last few years.

- Credit rating: California, Hawaii, Massachusetts, and Michigan have made it illegal for insurers to use your credit score as a factor in your rates. But if you live in any other state, your score has a major effect on your premiums. Most banks and credit unions now provide this information online, but if not you can also use one of several free services to see your score.

- Other drivers’ information: If you share your vehicle with other drivers in your family, you’ll have to share information about them, too. It will be the same kind of info you’ve shared about yourself.

2. Determine Your Car Insurance Budget

Cost is understandably one of the first concerns for most people when they shop for auto insurance. Since drivers in most places are required by law to carry an insurance policy, missing a payment can put you in legal jeopardy. That means that you want to get a realistic idea of what you can afford to pay for coverage so that you don’t risk not being able to make payments.

How Much Does Car Insurance Cost?

The national average rate for full-coverage auto insurance is $1,983 per year or around $165 per month. Most experts recommend full coverage policies because they protect you from financial risk.

However, you don’t need full coverage. You are only legally required to carry the insurance mandated by state minimum requirements – usually liability insurance and, in some cases, some additional coverage.

Minimum coverage policies are typically the cheapest car insurance that you can buy, but they leave you exposed to financial risk. Depending on where you live, you can find minimum coverage for as little as $30 to $40 per month.

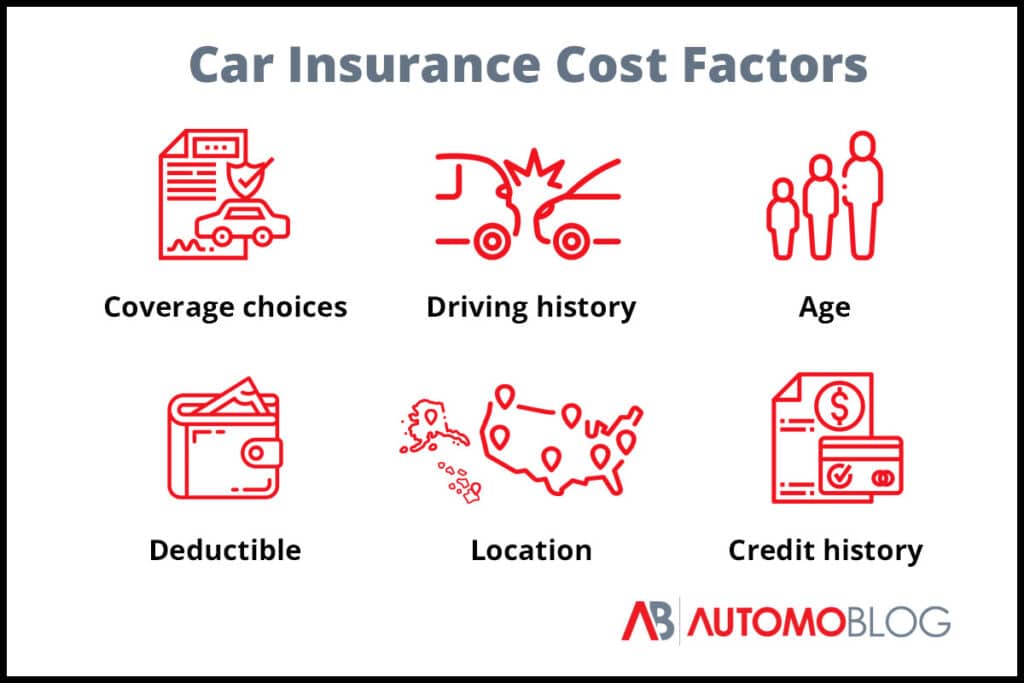

Car Insurance Cost Factors

Your rates will likely be different from the averages quoted above. That’s because insurers calculate individual rates based on a few different factors, including:

- Vehicle: Generally speaking, expensive cars cost more to insure.

- Deductible: A higher deductible will usually come with a lower rate.

- Coverage types: Minimum coverage policies will have the lowest premiums. Adding more coverage and policy add-ons will increase your rates.

- Coverage limits: The amount of coverage you have on your policy is also a factor. Choosing higher limits offers more protection but will raise the cost of your premium.

- Age: Insurers charge the highest premiums to young drivers (teen drivers, especially) and senior drivers.

- Location: Car insurance rates vary from one place to another. Even within the same state, your rate might be higher if you live in an urban area.

- Credit history: In states where insurers can use your credit score as a factor drivers with good credit scores will get better rates on their car insurance policies. People with fair or poor credit scores often pay much higher rates.

- Driving history: Your driving record plays a significant role in determining your rates. A recent at-fault accident, DUI, or traffic violation such as a speeding ticket could make your rates much higher.

Car Insurance Discounts

Another factor in your car insurance premium is any discounts you’re able to apply. Auto insurance providers typically offer at least a few discounts that can help make coverage more affordable. Some of the more common discounts include:

- Autopay: If you set your monthly payments to autopay, you may get a discount.

- Military: Some companies offer discounted rates to active and retired military members and their families.

- Safe driver: If you go for a long stretch without accidents or violations, you may be eligible for a discount.

- Anti-theft: You may be eligible for a discount if you have a car alarm or other anti-theft device on your vehicle.

- Good student: Some insurance companies offer discounts to students who maintain good grades in school.

- Senior: While senior citizens often pay higher premiums, some companies discount policies for people over 65.

- Safety features: Driving a vehicle with advanced safety features such as anti-lock brakes can earn you a discount.

- Paid in full: If you pay your entire annual premium up front instead of monthly, your company may reward you with a discount.

- Multi-policy: If your auto insurance company sells homeowners insurance, renters insurance, or life insurance, you can usually get a discount by bundling one or more of these policies with your car insurance.

Average Cost of Car Insurance in Each State

The rates in auto insurance quotes vary highly between states because of differing laws about required coverage and required coverage amounts. Average rates also vary due to the presence of different risk factors.

Here are the average rates for different kinds of car insurance across different states nationwide:

| State | Average Liability Coverage | Average Full Coverage |

| Alabama | $559 | $1,717 |

| Alaska | $642 | $1,629 |

| Arizona | $596 | $1,680 |

| Arkansas | $498 | $1,711 |

| California | $449 | $1,293 |

| Colorado | $641 | $2,177 |

| Connecticut | $1,070 | $2,229 |

| Delaware | $1,345 | $3,011 |

| District of Columbia | $632 | $1,795 |

| Florida | $1,707 | $3,991 |

| Georgia | $816 | $1,850 |

| Hawaii | $1,196 | $3,131 |

| Idaho | $372 | $1,035 |

| Illinois | $624 | $1,859 |

| Indiana | $506 | $1,407 |

| Iowa | $339 | $1,424 |

| Kansas | $585 | $1,681 |

| Kentucky | $628 | $1,803 |

| Louisiana | $1,139 | $3,429 |

| Maine | $427 | $1,062 |

| Maryland | $1,561 | $2,699 |

| Massachusetts | $530 | $1,836 |

| Michigan | $1,638 | $3,642 |

| Minnesota | $845 | $2,272 |

| Mississippi | $542 | $1,549 |

| Missouri | $540 | $1,758 |

| Montana | $485 | $1,773 |

| Nebraska | $427 | $1,483 |

| Nevada | $1,323 | $3,180 |

| New Hampshire | $514 | $1,244 |

| New Jersey | $1,371 | $2,345 |

| New Mexico | $636 | $2,134 |

| New York | $1,886 | $3,371 |

| North Carolina | $567 | $1,527 |

| North Dakota | $428 | $1,326 |

| Ohio | $632 | $1,408 |

| Oklahoma | $635 | $2,006 |

| Oregon | $818 | $1,497 |

| Pennsylvania | $860 | $3,255 |

| Rhode Island | $1,188 | $2,440 |

| South Carolina | $816 | $1,775 |

| South Dakota | $353 | $2,198 |

| Tennessee | $508 | $1,495 |

| Texas | $825 | $2,246 |

| Utah | $976 | $1,988 |

| Vermont | $318 | $978 |

| Virginia | $597 | $1,390 |

| Washington | $598 | $1,487 |

| West Virginia | $496 | $1,595 |

| Wisconsin | $617 | $1,962 |

| Wyoming | $329 | $1,479 |

3. Decide On Your Auto Coverage Needs

Once you have a good idea of your auto insurance budget, you can start figuring out which kinds of coverage you need and want on your policy. Companies offer standard insurance that takes care of basic coverage needs and options and add-ons that can cover other costs related to owning and driving your vehicle.

Standard Car Insurance Coverage

The standard items you’ll find at almost every insurance company offer basic liability coverage along with personal injury and property coverage. You can stick to your state minimum requirements or combine these items to make a full-coverage auto insurance policy. These include:

- Property damage liability insurance: Covers the cost of damages to other vehicles and property in an accident you’re found at fault for.

- Bodily injury liability insurance: Covers medical bills and other injury-related costs for other parties resulting from an accident in which you are found at fault.

- Collision coverage: Covers the cost of repairing damages if you’re involved in an accident with an object or another car.

- Comprehensive coverage: Covers damages from incidents other than collisions, such as natural disasters, theft, civil unrest, and vandalism.

- Medical payments (MedPay): Covers medical costs for you and your passengers regardless of who is at fault in an accident. Some no-fault insurance states require this coverage.

- Personal injury protection (PIP): Covers medical expenses similar to MedPay, but also compensates for other losses related to those injuries, such as wages lost due to being unable to work. Some states with no-fault insurance provisions require this type of coverage.

- Uninsured motorist or underinsured motorist coverage (UM/UIM): Covers you and your vehicle if you get into an accident with an at-fault driver who lacks adequate insurance to do so. Some states require this coverage.

Additional Coverage Options

You can also add supplemental insurance to your policy to help cover some of the other costs that may result from an accident or other loss. These options vary between different companies, but some of the most popular options include:

- Rental car reimbursement: Covers the cost of a rental car for you to use while your vehicle is out-of-use following a covered loss.

- Roadside assistance: Covers the cost of towing, fuel delivery, tire repair, and other emergency roadside services.

- Guaranteed asset protection (GAP) insurance: Covers some or all of the difference between what you owe your lender on your vehicle and its assessed value in the event of a total loss.

- Trip interruption: Covers lodging, food, and other related expenses if you can’t use your vehicle due to an accident or other loss while you’re away from home.

- Rideshare coverage: Covers your vehicle while you are working for a rideshare service such as Lyft or Uber but not actively carrying a passenger.

Many companies offer far more options than this. You can find listings of add-ons and coverage options on a provider’s website or in our reviews. Local insurance agents will also be able to tell you all of the options available to you.

4. Shop Car Insurance Providers

Now that you know what you’re looking for in a policy, you can start comparing providers. This is likely the most time-consuming step, but it’s also one of the most important. There can be major differences between providers in terms of the prices, services, and support they offer – even for identical policies.

How To Get Car Insurance Quotes

Shopping for auto coverage is much more efficient than it used to be, thanks to the ability to get and compare car insurance quotes quickly and easily. These days, you have a few ways to get free car insurance quotes.

- In person: You can always go the old-fashioned way and visit an insurance office to get quotes. This isn’t the most efficient way, but it allows you to speak with an agent about your options directly. Some independent brokers can give you quotes from multiple insurers.

- Over the phone: Auto insurance companies can provide you with a quote over the phone. This can also be a slow process compared to other options, but you’ll have the chance to ask an agent any questions you might have.

- Online: The fastest and easiest way to get car insurance quotes is to do it online. Companies typically have forms to request quotes, but you can also find online comparison tools that let you get multiple quotes at once, making it easy to compare options.

Comparing Car Insurance Providers: What To Consider

The cost of your auto policy is likely your first concern, but it shouldn’t be your only one. Not all providers offer the same level of service. Low-quality providers may be difficult to deal with when you need to file a claim or lack adequate support for customers.

There are a few things to look out for in a provider in addition to the price they quote you, including:

- Industry reputation: Organizations like the Better Business Bureau (BBB), the National Association of Insurance Commissioners (NAIC), J.D. Power, and AM Best all offer independent evaluations of insurance companies. Companies with strong ratings from these organizations are generally trustworthy, while those with poor ratings may not be reliable service providers.

- Customer satisfaction: You can find customer reviews for insurance providers in many places on the internet, including Google, the BBB, and TrustPilot. While customer ratings tend to skew negative since people are more likely to post complaints than compliments, you should pay attention to any consistent patterns you find in these comments.

- Technology: Most insurers offer an online interface for managing your policy, reporting claims, and more. Many offer them in the form of mobile apps, too. These options make dealing with your insurance policy more convenient, so you’ll want to consider the ease of a company’s online experience in addition to whether or not they have one to begin with.

- Other insurance products: Many auto insurers also sell other insurance products, such as umbrella, life, and home insurance policies. Having all of your insurance policies in one place can make it much more convenient to deal with them, and many providers offer a discount for bundling your services. Consider which insurance products you have or will need in the near future and whether a provider offers them.

- Service options: Some insurance companies are able to offer lower rates because they have limited in-person offices or none at all. That may be fine for people who prefer to take care of insurance matters online or over the phone. But if being able to deal with issues in person is important to you, you should consider whether an insurer has offices that are convenient for you.

How To Compare Auto Insurance Providers

Between the quotes you receive and the other criteria you use to evaluate providers, comparing car insurance companies can be time-consuming if you try to do it on your own. Thankfully, you don’t need to.

Our team of experts conducts an annual auto insurance study that spans the entire industry. We look into dozens of providers and their coverage, analyzing thousands of rate estimates, hundreds of ratings from multiple organizations, and countless customer reviews to get an accurate picture of the cost and quality of each company.

You can see our findings in our round-ups of the best car insurance companies and follow up on insurers that catch your attention with our in-depth provider reviews. This can help you gain a better understanding of the insurance industry and narrow down your options to a few providers that fit your needs.

5. Decide On a Provider and Policy

After assessing your options, it’s time to make a decision about your car insurance. The best provider for you will be the one that offers you the lowest rates on the policy you want while giving you confidence that they will be there when you need them.

While you can usually complete this process online, it may be helpful to work with an agent. They can help you make sure that you’ve got all the options and coverage limits you want and that you’ve applied every discount available to you.

How To Pay For Car Insurance

Once you’ve made a decision, you’ll need to make your first premium payment. You can pay this premium over monthly payments, but you can also choose to pay it all at once. Paying your entire premium upfront can usually get you a discount on your policy.

If you choose to go with monthly payments, you may still be able to get a discount or two. Many providers offer a discount for getting your bills and communications electronically instead of through the mail. You can also often get a discount for setting up automatic payments.

How To Get Cheaper Car Insurance Rates

There isn’t much you can do about some of your rate factors, like your age, location, and driving record. However, there are a few things you can do to try to lower your premiums, both immediately and in the future, including:

- Shop around for car insurance: Getting quotes and considering multiple options is essential to finding the best provider and rates.

- Increase your deductible: A higher deductible means you’ll have to pay more out-of-pocket towards an insurance claim, but it’s a good way to lower your premium immediately.

- Complete a driving course: Many insurers offer a significant discount for completing a defensive driving course approved by the company or your state agency. These classes can also improve your driving skills and reduce the risk of an accident or violation.

- Try usage-based insurance: Some insurers offer insurance policies that charge by the mile instead of a flat rate. If you don’t drive much or can reduce how much you use your car, you may be able to save on coverage.

- Use a telematics program: Another alternative to flat-rate auto policies are the increasingly-popular telematics programs. These programs monitor your driving behavior with a mobile app and reward consistent safe driving behavior with lower rates. However, they can also increase your rates if you aren’t careful.

- Consider smaller providers: In our insurance study, we found that some of the best rates came from smaller regional providers that are easy to overlook. Try to include a few of these providers in your search to see if they can offer you better rates than the large national insurers.

Shop Car Insurance: Conclusion

The difference between the right auto insurance provider and the wrong one can be miles apart in both the service you receive and the price you pay. Taking an organized approach when you shop for car insurance can help ensure that you get the coverage you want from a provider you can trust at a price you can be happy with.

No one car insurance company is the best provider for every driver. The insurer that makes the most sense for your neighbor may not be the right choice for you. When you shop car insurance providers, keep your own needs and preferences front and center and take the time to compare and consider multiple options.

Shop Car Insurance: Recommended Providers

The best insurance provider for you will depend on your own unique profile, coverage needs, and budget. That’s why it’s important to get quotes from several insurers and compare. However, you’ve got to start your search somewhere. We recommend getting started with two of the highest-scoring companies in our most recent auto insurance study.

State Farm: Best Customer Experience

State Farm earned the highest overall score in our study, winning the nation’s largest insurer the title of Best Overall for this year. The provider offers a winning combination of competitive rates, a wide range of coverage options, a large selection of discounts, and one of the best reputations in the industry. State Farm also has more than 18,000 local insurance agents to provide in-person service in all 50 states – more than any other provider. The company is likely to be a strong option for most drivers.

Keep reading: State Farm car insurance review

GEICO: Most Discount Options

GEICO features a wider and more diverse collection of auto insurance discounts than almost any other provider in our study, earning it this year’s award for Best Discount Selection. Nearly every driver can find at least one discount they can apply. But throughout our study, GEICO consistently offered some of the lowest rate estimates in most markets as well. That means drivers can apply those discounts on top of already-low rates, making GEICO a good option for people in search of cheap car insurance from a reputable provider.

Keep reading: GEICO car insurance review

Shop Car Insurance: FAQ

Does shopping for car insurance hurt your credit?

No, shopping for car insurance does not hurt your credit score. Companies check your credit score to help determine your rates, but they use a “soft pull” of your credit, which doesn’t affect your score.

Is it cheaper to have business car insurance?

No. Business car insurance is usually more expensive than consumer car insurance. That’s because more significant risks are involved, and there’s a greater chance that more than one driver will use the vehicle.

Is it OK to buy car insurance online?

Buying car insurance online is easy and fast and sometimes even gets you discounts. It’s also safe, for the most part. However, since you will be handing personal information over, be cautious if you buy your car insurance online.

Does it hurt your credit to shop for car insurance?

It should not hurt your credit to shop for car insurance. While your credit score may be a factor in your rates, insurers should use a “soft credit check” that does not impact your score.

Is it good to shop around for insurance?

It is always good to shop around for insurance, even if you’re satisfied with your current provider. Rates change regularly, so the provider that offered you the lowest premiums last year may not have the best rates now.

Which company gives cheapest car insurance?

Based on our research, GEICO and State Farm tend to give the cheapest car insurance rates among national providers available to the general public. USAA often offers cheaper rates, but it is only available to military members, veterans, and their families.

Drivers in certain situations may find cheaper rates with other providers, too. For example, Progressive is often the cheapest option for drivers with a DUI. Shopping around for car insurance can help you make sure you’re getting the lowest rates.

How often should you shop car insurance?

At a minimum, you should shop for car insurance whenever you are getting close to renewing your policy – typically once every six months or a year. However, you can shop for car insurance whenever you have the time for it, and doing so might reveal a better deal than you currently have.

Our Methodology

Our expert review team takes satisfaction in providing accurate and unbiased information. We identified the following rating categories based on consumer survey data and conducted extensive research to formulate rankings of the best car insurance providers.

- Affordability: A variety of factors influence cost, so it can be difficult to compare quotes between providers. Our team considers auto insurance rate estimates generated by Quadrant Information Services and discount opportunities when giving this score.

- Coverage: Because each consumer has unique needs, it’s essential that a car insurance company offers an array of coverage options. We take into account the types of insurance available, maximum coverage limits, and add-on policies.

- Industry Standing: Our team considers Better Business Bureau (BBB) ratings, financial strength, and years in business when giving this score.

- Availability: Auto insurers with greater state availability and few eligibility requirements are more likely to meet consumer needs.

- Customer Service: Reputable car insurance providers operate with a certain degree of care for consumers. We consider complaints filed with the National Association of Insurance Commissioners (NAIC), J.D. Power claims servicing scores, and customer feedback.

- Online Experience: Insurers with easy-to-use websites and highly rated mobile apps scored best in this category.