Affiliate Disclosure: Automoblog and its partners may earn a commission when you use the services or tools provided on site. These commissions come to us at no additional cost to you. See our Privacy Policy to learn more.

After more than a year of sharp, steady increases, used car prices started falling in the late summer of 2022. The drop in prices has already had wide-reaching effects around the auto industry, but a difficult supply chain situation and higher interest rates makes it hard to predict what that drop could mean for the average car buyer.

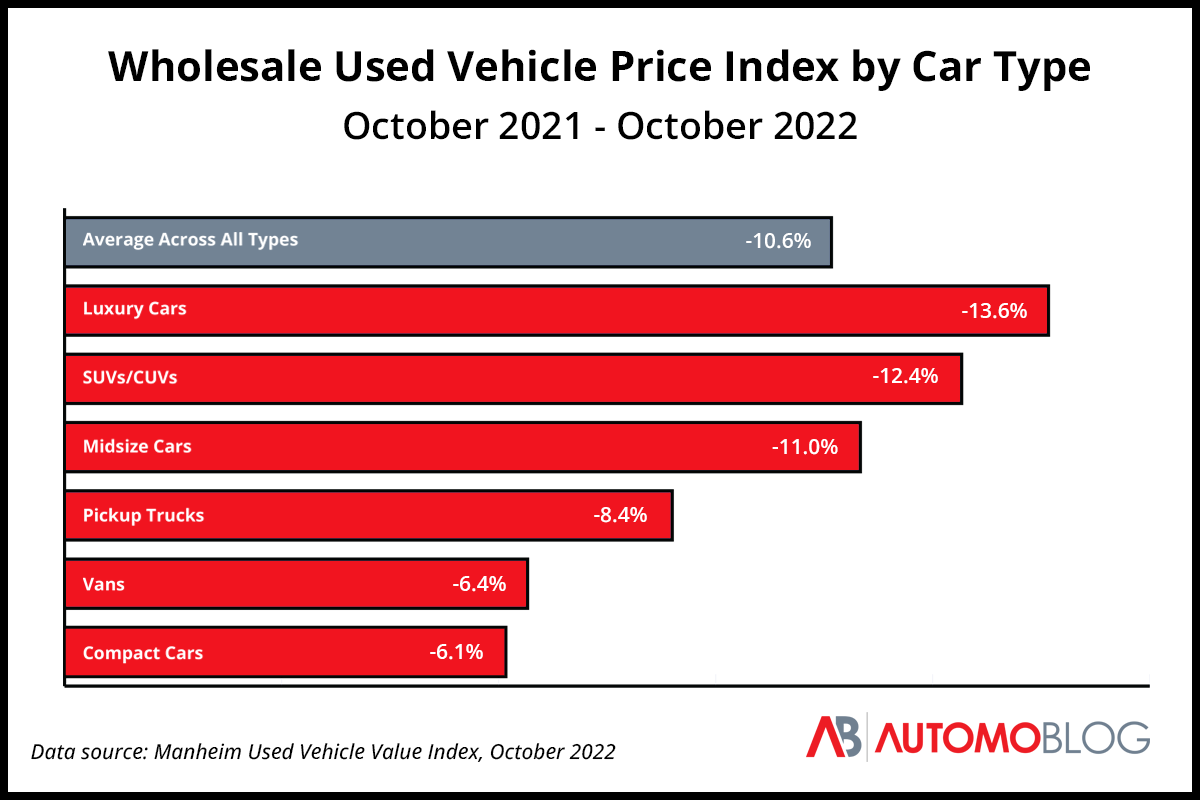

Used Car Prices are Falling Fast – At the Wholesale Level

Rapidly falling used car prices may be the headline, but the reported drop is based mainly on the wholesale prices of used vehicles.

According to the Manheim Used Vehicle Index – a proprietary metric that accounts for average pricing of vehicles, taking into account differences in make, model, body type, model year, and mileage – the wholesale price of used cars reached its peak at the end of 2021. The index fell slightly during the first quarter of 2022 before leveling out for a few months.

After July of 2022, wholesale used car prices started to see a more severe drop. Between July and August, the Manheim Index fell more than 4%, a rate that has roughly continued since. The October index of 200 marks a 15% decrease from its January peak of 236.3.

Dropping Price Percentage Varies by Vehicle Type

The average drop in used car prices year-on-year from October 2021 to October 2022 was 10.6%, according to the latest Manheim report. However, the decrease in used vehicle prices varied between different types of cars.

Luxury vehicles saw the biggest drop among all vehicle types, with prices falling 13.6%. The next category of vehicles was SUVs and crossovers (CUVs), which saw prices fall 12.4%. Compact cars saw the smallest decrease, with prices falling 6.1% over the last year.

Why Are Used Car Prices Dropping?

A major reason that used car prices were previously so high is supply issues. Since the beginning of the pandemic, the chip shortage and other supply chain issues reduced the supply of new vehicles, resulting in increased demand for used vehicles.

With those issues showing signs of easing, the supply of used cars has begun to increase. According to one report from Kelley Blue Book (KBB), used car inventory sat at 2.46 million nationwide at the end of August. This roughly matched the inventory from a month earlier, signaling a greater supply of used vehicles compared to previous months.

Chris Frey, Cox Automotive’s senior manager for Industry Insights, spoke to KBB about the change in used car supply, saying, “Inventory volume at the end of August was 10% above year-ago levels, so we’re seeing some improvement.”

Lower Wholesale Prices Aren’t Necessarily Making Used Cars More Affordable

While used car prices are falling for wholesalers, that doesn’t necessarily translate to more-affordable vehicles for individual car buyers. Car dealers may pay less for used vehicles, but that doesn’t mean they’ll lower their asking prices. Despite the latest drop in wholesale prices, retail prices for used cars are still 7.2% higher than the same time last year, according to data from the Bureau of Labor Statistics (BLS).

Even if retail prices eventually drop along with wholesale price trends, other factors mean that used cars are less affordable now than they have been.

Rising Interest Rates Can Counteract Falling Used Car Prices

The Federal Reserve issued a series of rate hikes to the federal funds rate beginning in March in an attempt to counter inflation. At the beginning of 2022, the federal funds rate sat at around 0%. After six rate hikes, it now sits at 3.75% to 4.0%. This has resulted in a dramatic increase in auto loan rates, both for used and new vehicles.

According to industry data, the average rate for a 60-month loan on a new car jumped from 3.85% in January, 2022 to 5.16% in September. More recent data for used car loan rates was not available at the time of publication.

This 34% increase in the average interest rate represents a difference that can change the affordability equation for some buyers. According to a report from the National Automobile Dealers Association (NADA), the average transaction price for a used car in September 2022 was $31,025. Using this as an example, we can see how the increase in interest rates changes the total price and monthly payments for a vehicle.

| Purchase Price | Interest Rate | Monthly Payment | Total Cost | Interest Cost |

|---|---|---|---|---|

| $31,025 | 3.85% | $569.27 | $34,156.49 | $3,131.49 |

| $31,025 | 5.16% | $587.76 | $35,265.42 | $4,240.42 |

This difference in total cost and monthly payments can be even greater when it comes to used car loans, as these may vary much more than loans for new vehicles. The cost difference between loan rates is also exacerbated when borrowers take on longer loan terms, which has become a trend in recent years.

Inflation Has Decreased Overall Affordability For Many Car Buyers

The Federal Reserve’s rate increases were implemented to try and tame runaway inflation. While, according to BLS data, the rate of inflation has slowed – the consumer price index (CPI) rose by only 0.4% in October – the CPI is still 7.7% higher than a year ago across major categories.

The rising costs of living have not coincided with higher wages, which have not seen a meaningful increase over the same period of time. This means that workers are spending a larger portion of their income on goods and services, leaving less room in the budget for car payments and increasing the challenge of saving for a down payment.

Rising Interest Rates Can Result in Higher Debt Payments

The increase to the federal funds rate hasn’t just resulted in higher interest rates for auto loans. According to data from Bankrate, the national average annual percentage rate (APR) for credit cards increased by 2.74% in 2022. This means borrowers are effectively paying more towards credit card debt overall and are likely to have higher monthly payment requirements.

Mortgage rates have also increased significantly. In early November, rates reached an average of 7% for the first time in more than two decades. While they have since dipped just below that figure to an average of 6.95%, the higher rates can mean a significant increase in monthly mortgage payments, both for new buyers and for current mortgage holders with adjustable rate mortgages (ARMs).

Monthly debt obligations are part of the debt-to-income (DTI) ratio lenders use to determine the monthly auto loan payments – and therefore overall purchase price – a borrower can afford. Without a corresponding increase in salary, a borrower’s debt obligations account for a larger portion of their income, thereby decreasing their purchasing power.

Falling Used Car Prices: Is Now a Good Time to Buy?

Despite the recent trend of falling used car prices at the wholesale level, it’s still not an ideal time to buy a used vehicle.

Actual Sales Prices Still Haven’t Gone Down

As mentioned before, falling wholesale prices of used cars hasn’t yet translated into lower sticker prices at dealerships. While wholesale prices started to come down towards the end of July and beginning of August, the average used car transaction price remained at an all-time high as of September, according to data from NADA.

Experts like Mark Schirmer, director of public relations with Cox Automotive, predict that prices will remain relatively steady in the near future. “We still think that with new vehicle inventory still low, we’re not expecting retail prices or wholesale prices to crash, but we certainly expect for them to come down some,” he said in an interview with The Hill. “We’re not expecting a huge correction. They’re going to stay historically elevated for a while.” For reference, Cox Automotive is the company that publishes the Manheim Used Vehicle Index.

Based on what Schirmer is saying, the price of used cars is likely to remain high for the near future. While that means people buying now will pay more than they would have even a year ago, it also means that those looking to hold out for substantial retail price drops may be waiting for a long time.

Interest Rates Are Still High

For those who need to borrow money to purchase a used vehicle, higher interest rates mean paying more for a loan overall. This means paying more in interest on top of paying an inflated price for a used car.

However, auto loan rates for new and used vehicles are likely to continue to climb through 2023. In September, San Francisco Federal Reserve Bank President Mary Daly told reporters that she believes the Federal Reserve will raise the federal funds rate again – up to around 4.5% this year, and next year up to around 5%. She suggested that the goal is to then keep the funds rate around 5% throughout the year before potentially bringing it back down starting in 2024.

So while auto loan rates for used cars are indeed much higher now than they have been in the recent past, they are also not likely to drop any time soon. That means that people who need a loan to buy a used car may have access to the best rates now than they will for a while.

Automotive Supply Chain Issues Are Unpredictable at Best

One of the major drivers of the enormous increase in used car prices over the last two years has been supply chain issues that have limited the stock and delivery of new vehicles. Many predict that the vehicle chip shortage – perhaps the most pressing of the auto supply chain problems – will continue through 2023.

Many automakers have worked to develop sourcing alternatives to try and alleviate some of their supply issues. Manufacturers have also made investments in domestic plants that could reduce dependency on foreign producers and international logistics.

But while these strategy shifts and investments could indeed help to create a more robust and reliable supply chain in the long term, it’s unlikely that it will bring an end to current issues in the near future.

According to Auto Forecast Solutions’ (AFS) estimates, shutdowns, delays, and other issues have resulted in a loss of more than 3.5 million vehicles globally in 2022. Regardless of what improvements may come in 2023, it is unlikely that new vehicle supply will return to “normal” in the next calendar year.

For people thinking of buying a pre-owned vehicle, this means that used cars will still be supplementing the lack of new cars for the time being. As a result, sticker prices aren’t likely to budge much at the consumer level.

Do Falling Used Car Prices Mean You Should Buy Now?

The short answer to whether or not it’s a good time to buy a used car is no, not unless you have to. A highly competitive market, record average prices, and high interest rates mean that now is one of the most expensive times to buy a used car in recent history. In short, falling used car prices at the wholesale level have yet to translate to good deals at the used car lot.

Despite the current unsuitable conditions, there are some reasons why people in need of a vehicle might want to purchase a used car at this time, rather than wait. Even higher interest rates are on the horizon, and there are no clear signs of sticker prices dropping anytime soon. So, now may be as good of an opportunity to buy a used car as one may have for some time to come.