Affiliate Disclosure: Automoblog and its partners may earn a commission when you use the services or tools provided on site. These commissions come to us at no additional cost to you. See our Privacy Policy to learn more.

In November of 2022, the Consumer Financial Protection Bureau (CFPB) announced that it would be launching an auto finance data pilot program to collect and analyze more data from the industry. After meeting with various stakeholders over the following months, the bureau released a statement detailing the launch of the program on February 23, 2023.

The announcement comes at a critical time for automotive finance. A quick drop in the price of used cars following all-time high sticker prices has left millions of people underwater on their car loans. Continued hikes to the federal funds rate mean that auto loan interest rates keep going up. These issues and others are part of a rapidly-evolving finance market that’s sparking concerns among regulators.

Automoblog spoke with officials at the CFPB on an informational call in March to learn more about the program, the reasons for launching it, and its goals. Here’s what we learned.

What is the CFPB Auto Finance Data Pilot?

In short, the CFPB auto loan data pilot is a new program designed to collect more detailed data about the auto finance industry. The program was first announced in November 2022.

To collect that information, the CFPB is working directly with nine consumer auto lenders. According to a CFPB press release, these nine lenders represent a cross-section of the auto finance market, so their data should provide a well-rounded view of the industry.

The Pilot Addresses a Number of Issues with Auto Loan Data

One of the primary reasons for launching the pilot, according to our source and the CFPB press release, is the current lack of data around auto lending. With an estimated $1.5 trillion in outstanding loan debt in the U.S., auto lending is the third-largest consumer credit category behind mortgages and student loans.

But despite the size of the market, the CFPB says that there is a large gap between the amount of information they have about mortgages and student loans and what they have about auto loans. Financial analysts and regulators have long had detailed information about mortgage lending, and the federal government administers student loans, so it has direct access to that data. In comparison, information about auto lending is relatively sparse.

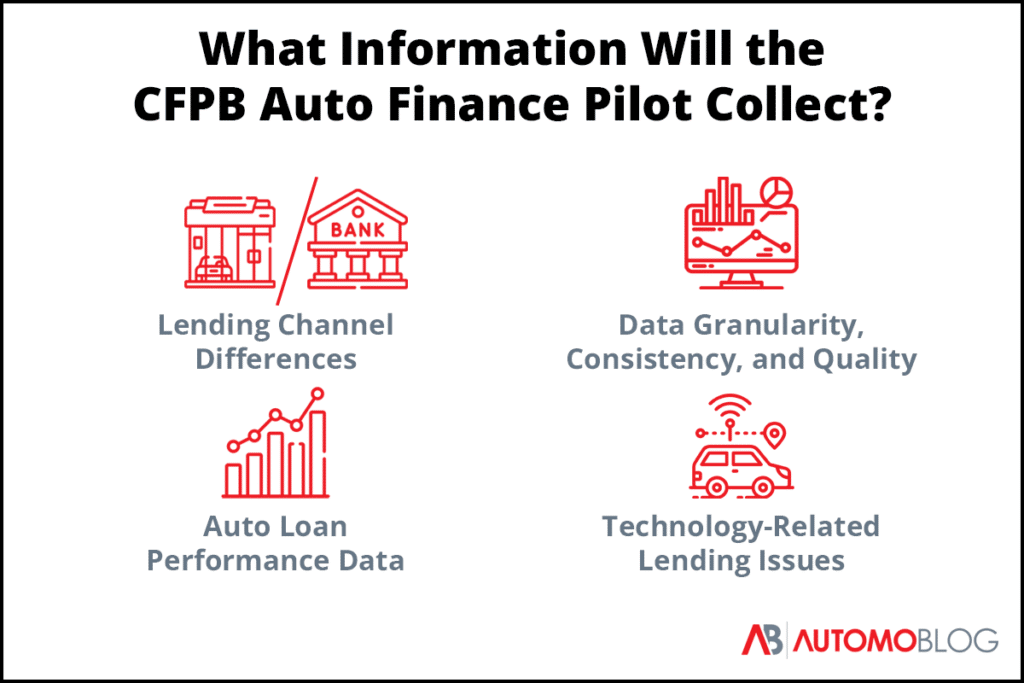

In its press release, the CFPB identified several issues with the current state of automotive finance data. The group broke down the three areas that stakeholders indicated could benefit from additional data visibility: data granularity, consistency, and quality; loan performance trends; and lending-related issues, such as the use of certain technologies.

Lending Channel Differences

One of the key issues with the present auto lending data is a lack of segmentation. Auto loan data isn’t typically broken down by whether a borrower finances a purchase through direct or indirect lending.

In a direct lending model, the borrower works with a lender to secure the funds needed to make a purchase or refinance a loan. Indirect lending refers to when a car dealer finds financing for the borrower.

The differences between these lending channels in terms of loan terms, interest rates, and other details can be substantial. As a result, the lack of differentiation in data collection makes it difficult to gain a nuanced understanding of the loan market with respect to these channels. With the data pilot, the CFPB can analyze these channels separately.

Data Granularity, Consistency, and Quality

Our source at the CFPB said that a general lack of granularity around loan data is another problem that they hope to solve with the pilot. Loans are individualized in nature. Lenders base rates and terms on borrowers’ credit scores and other factors. Yet these granular details are not always accounted for in auto finance data, muddying the results.

The lack of consistency and varying quality of that information is also an obstacle to analysts and regulators. According to the CFPB, this is due to how auto loan data has been collected and distributed until now.

Much of the data around auto loans is proprietary – or, owned by a private party. This creates several problems for analysts and regulators. The lack of a centralized data set means that just gathering automotive loan data is more time-consuming and difficult than it is in other industries.

But it also means that there can be variations in the terms and definitions parties use in their data collection and analysis. Different providers may, for example, have varying score ranges for credit categories. One provider may define the “prime” category as ranging from 660 to 719, while another may define that category as ranging from 640 to 700. As a result, one provider’s data set would be incompatible with the other’s without controlling for these differences.

By creating a centralized data set, the pilot program can improve the quality and consistency of available auto finance data.

Loan Performance Trends

With auto loan default rates nearing all-time highs, loan performance is a key issue for the CFPB. The lack of reliable information on repossessions was a key point in the bureau’s February press release. This includes information such as how long a loan is past due before a car is repossessed, or how long a borrower has paid on a loan before their car is repossessed.

But the press release also indicates an interest in more specific information about which borrowers are facing higher default and repossession rates. It mentions a need for more data around the correlations between delinquency rates and demographic factors such as credit score, geography, and income, as well as how repossession impacts borrowers and lenders.

Related Lending Issues

The scope of the pilot extends beyond data about auto loans themselves. Adjacent issues such as the use of GPS tracking and starter-interrupt devices by lenders are also an area of interest for the CFPB.

Through this research, the bureau could gain more insight into how and how often these technologies are used by lenders and dealers. It could also provide insight into the impact they have on liability, privacy, and security concerns.

What the CFPB Auto Finance Data Pilot Means For You

The new data pilot is still in its infancy. Officials at the CFPB are only beginning to collect what will surely be a massive amount of data about automotive finance. And even when that data is collected, it may be some time before the general public has access to it.

Automoblog was told that initially, the findings from the pilot won’t be made publicly available. However, the CFPB may publish summary information about its key findings after conducting its analysis.

The collection and centralization of higher-quality, more consistent, and more granular finance data will provide valuable insight into the country’s third-largest credit market. Down the road, those insights could eventually help the CFPB and others to craft regulations to help protect borrowers from predatory lending practices and other dangers related to auto loans.

In the opening paragraph of its February 23 press release, the CFPB called out the disproportionate impact of the recent rise in auto loan delinquencies and the affordability crisis on people with lower incomes and credit scores.

“Recent data show an increase in auto loan delinquencies, particularly for low-income consumers and those with subprime credit scores,” it says. “Some consumers may even be getting priced out of the current market.”

The auto finance data pilot could help the CFPB better understand these trends. Eventually, that data may help it improve them.